The Export-Import Bank of the United States (EXIM) is an increasingly significant tool in the U.S. government’s foreign and industrial policy toolkit. The administration is pursuing large-scale investments, such as the critical minerals focused Project Vault, and Congress is working to extend and improve EXIM’s authorities.

But as we mentioned in our priorities for reform, increasing American competitiveness in globally strategic sectors like advanced energy requires EXIM to adjust its risk appetite. That adjustment, however, requires Congress to appropriate sufficient funds to cover the higher credit subsidy costs that come with expanded risk tolerance.

A significantly increased program budget is a vital element of unlocking EXIM’s full potential.

Federal Credit, Explained

EXIM’s financing activities, such as loans, loan guarantees, and insurance1, are part of a larger bucket of over one hundred “federal credit programs.” These also include programs, for example, at the Development Finance Corporation and the Department of Energy’s Office of Energy Dominance Financing (formerly the Loan Programs Office). Federal credit programs are governed primarily by the framework set out in the Federal Credit Reform Act of 1990 (FCRA).

To understand why this matters for EXIM’s ability to take on more risk, we first must understand the basics of FCRA.

Similar to how private financial institutions determine the value and profitability of a given transaction, FCRA directs that the cost of federal credit programs be determined on a net present value (NPV) basis. This means that, from a purely budgetary perspective, the up-front cost of a loan or guarantee is determined not by the dollar value of the transaction, but by the estimated present value of the long-term cost to the government over the life of the loan.

To determine the NPV basis, the agency issuing the loan or guarantee—in coordination with the Office of Management and Budget—builds a model weighing the risk of default against other factors, including the amount disbursed, loan tenor, scheduled repayments, interest payments and rates, and fees charged.

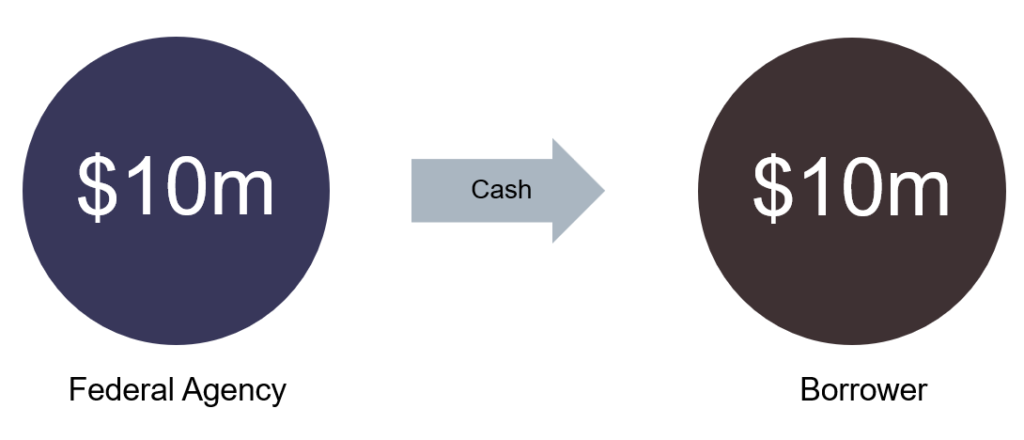

Let’s examine a theoretical $10 million direct loan made by a federal agency to see how this works.

In this example, the $10 million in cash is disbursed to the borrower on day one of the loan:

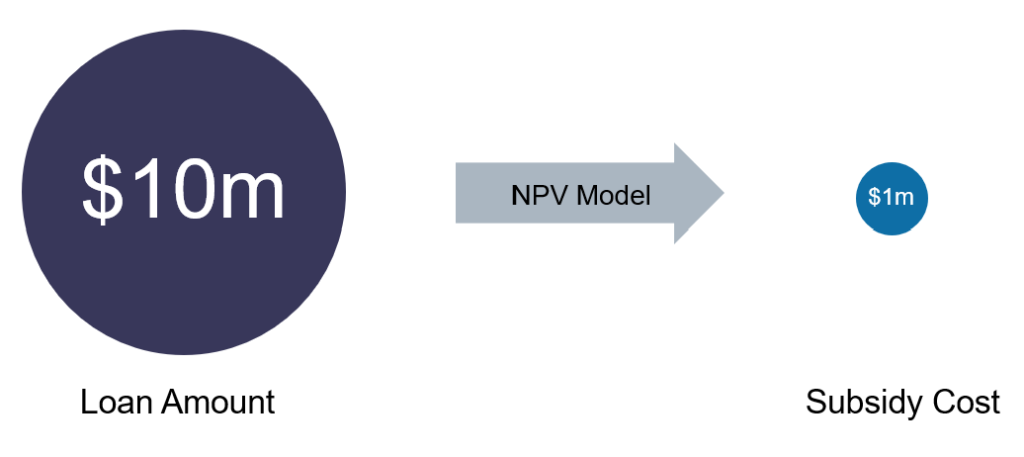

Because FCRA dictates that the loan be treated on an NPV basis and not a cash basis, the budgetary cost to the government is not $10 million.

Instead, the cost is determined by the model. Let’s say that after weighing all factors, including the risk of default, the NPV of the loan is negative $1 million, meaning that the risk of default outweighs the anticipated repayment flows. This is not an inherently undesirable outcome, especially for programs designed to finance projects that are too risky for the private sector to undertake on its own. These types of projects might be in higher-risk emerging economies, have long tenors, or carry concessional (below market) rates.

What it does mean is that, per FCRA, the government needs to account for the cost differential of the negative NPV through an up-front cost. This up-front cost to the agency is called a subsidy.

In this theoretical, the subsidy cost is $1 million, which accounts for the risk taken on by the government:

To “pay” this subsidy, the agency requires appropriated funding from Congress. If no such funding exists, agencies cannot support higher risk transactions.

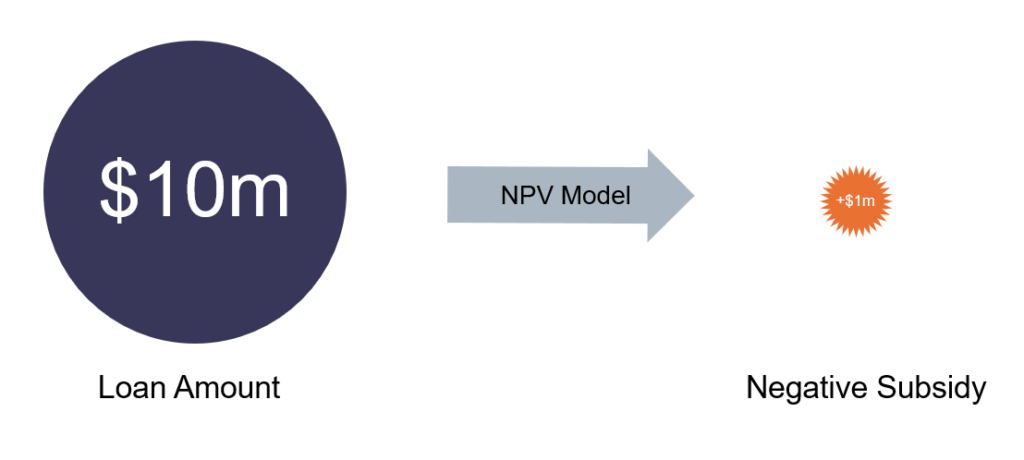

Further complicating things, sometimes a loan is so safe that the NPV of the transaction is positive: the present value of the loan is above zero, even accounting for the risk of default. This is often the case if a transaction is in a low-risk country, with an established borrower, shorter tenor, and non-concessional rates.

Let’s return to our theoretical loan. If the model indicates that this transaction is so low risk that its NPV is a positive $1 million, the agency does not have to use appropriated funds as subsidy.

Instead, it creates something called a negative subsidy—a net receipt that is remitted to the Treasury, reducing that agency’s net annual budgetary cost to the government:

EXIM’s Need for Subsidy

The majority of EXIM’s financed transactions have been so low risk that they have generated a negative subsidy, requiring no appropriated dollars. In Fiscal Year (FY) 2026, for example, EXIM projects that it will generate nearly $160 million in negative subsidy. This is often presented as a selling point for EXIM: its financing activities are so safe that they generate a reliable return for taxpayers.

EXIM must remain a good steward of taxpayer money and appropriately mitigate risk. It is also true that state-backed competition is on the rise globally. American businesses and workers need government support to help level the playing field overseas, especially in critical sectors and where the private sector is unable or unwilling to provide financing. Both the administration and some members of Congress have recognized this, seeking to make statutory changes through EXIM’s reauthorization to allow for higher-risk, higher-reward transactions. As they do this, they must not forget the essential role of appropriated funds. Statutory and administrative changes to right-size EXIM’s risk appetite will be toothless unless the bank has funds available for subsidy.

The FY 2026 enacted appropriations allow for up to $20 million to be used as subsidy for loans, guarantees, and insurance, a slight increase from the $15 million appropriated in FY 2025. In its FY 2027 budget request, however, the administration requested $200 million in program budget that could be used as subsidy, a ten-fold increase over existing levels, citing the need for EXIM to support transactions in critical minerals and transformational export sectors. If enacted, a program budget of this scale would enable EXIM to support these critical sectors. Unfortunately, the House FY 2027 National Security, Department of State, and Related Programs Appropriations Act, which passed out of committee in April, only provides $30 million in program budget. The Senate has not yet released appropriations text.

Program budget from Congress does more than enable higher-impact transactions—it signals permission to pursue them, even when there is higher risk. That congressional backing is key to overcoming institutional risk aversion within EXIM itself.

There is another, less direct, avenue by which EXIM can secure subsidy funds: special transfers from other agencies. While agencies have several mechanisms by which to transfer funds to other agencies—such as Section 632 of the Foreign Assistance Act—transferred funds can generally only be used for the same purposes for which they were originally appropriated. This means that funds appropriated for grant-based foreign assistance generally cannot be transferred to EXIM to be used as subsidy for a loan or guarantee. However, Congress can, and has, made exceptions to this rule.

In the Ukraine Security Supplemental Appropriations Act, 2024, Congress included a provision allowing some funds appropriated to the State Department and USAID to be “transferred to, and merged with” EXIM’s program account.2 By including these few words in appropriations text, Congress allowed transferred funds to take on the characteristics of EXIM’s program account, including allowing them to be used as subsidy for loans and guarantees. A similar provision has also appeared in the past several full-year appropriations bills, which allow funds appropriated for the Economic Resilience initiative (ERI) to be transferred to EXIM and used as subsidy. Additionally, recently proposed pieces of legislation, such as the DOMINANCE Act, include transfer and merge authorities from State to EXIM and other agencies.

It should be noted, however, that transfer authority is not a replacement for dedicated appropriations at EXIM itself. It leaves EXIM reliant on other agencies for high-impact transactions, and there is no guarantee that agencies will agree to transfer funds—especially in a resource-constrained environment. Financing is also not a replacement for other kinds of support, and excessive transfers may erode programs that promote economic and market development through other means.

Recommendations

There are several near-term steps Congress and the administration can take to enable higher-impact transactions at EXIM:

- Congress should include an authorization of appropriations for program budget in EXIM’s reauthorization, as both an acknowledgement of the essential need for subsidy and as a clear signal to appropriators.

- Congress should increase funding for EXIM’s program budget in the enacted FY 2027 appropriations bill, in line with the ambition of the administration’s request.

- The administration should responsibly utilize the transfer authorities associated with ERI funds and those provided through the DOMINANCE Act, if enacted.

1 Most federal insurance programs are considered loan guarantees for the purposes of FCRA.

2 Transfer and merge authority was also granted to transfers to DFC.