Policymakers are increasingly interested in understanding the complex, nuanced supply chains for critical minerals and in improving supply chain security. The status quo reflects that the U.S. is strikingly vulnerable. Today, the U.S. has limited production capacity, almost no processing capacity, and a growing advanced manufacturing sector with a ballooning demand for mineral inputs.

This leaves the U.S. with a high import reliance that is vulnerable to disruption. In 2024, the U.S. was 100% reliant on imports for 12 critical minerals, with an additional 28 having an import reliance greater than 50%.

Without substantial shifts in policy and clear market signals, the U.S. will have little control over the security of its critical minerals supply chain. The White House has recently taken a strong interest in securing U.S. critical minerals supplies in executive orders (e.g., March 20, April 15). Thus far, the administration has prioritized expanding domestic capacity and has indicated interest in extending efforts to include international cooperation.

This analysis aims to support these efforts by providing a diagnosis of the global market outlook.

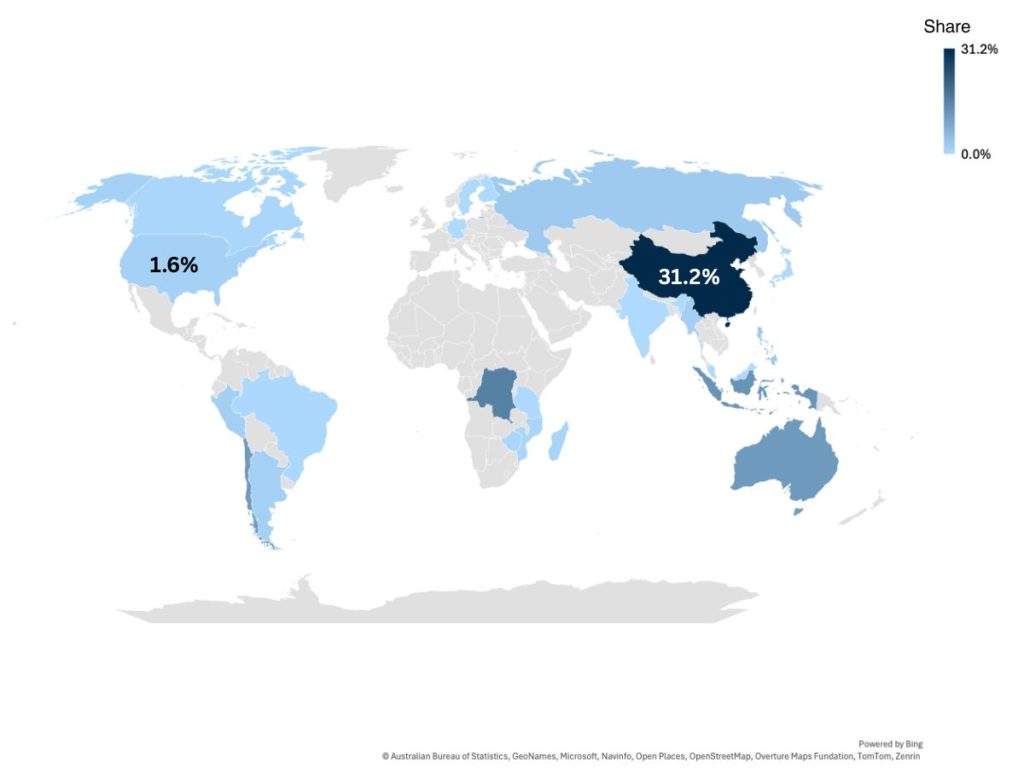

This visualization uses projections from the International Energy Agency to show mining and processing capacity by country in 2030 for six minerals essential to advanced energy technologies: copper, cobalt, lithium, nickel, rare earth elements, and graphite. The United States government classifies these minerals as “critical,” essential to economic, energy, or national security, and have a high disruption potential.

Figure 1. IEA Critical Mineral Market Share Outlook, 2030 (%)

China is the projected leader in 2030 with an average market share of 31% in the mining and processing of the six minerals covered by the IEA analysis. China has strategically embraced export restrictions, substantial subsidies, and market manipulation for decades to build and retain dominance over the marketplace. It has its strongest positions in graphite and rare earth elements (REE) mining and processing—crucial for batteries and advanced electronics.

The Democratic Republic of the Congo (DRC) is projected to have a market share of 15.7%. The DRC’s prominence is driven by copper and cobalt mining; it has limited processing capacity. Notably, China controls 72% of the DRC’s cobalt and copper mines, including the Tenke Fungurume Mine, which alone produces about 12% of the world’s cobalt.

Indonesia follows with a 12% market share, driven by its strong nickel mining and refining sector. Similar to the DRC, Chinese firms have a strong footprint on the ground, controlling an estimated 75% of Indonesian refining capacity—this is especially significant given the country’s ban on nickel ore exports.

The U.S. ranks 11th with a projected market share of 1.6% in 2030. Fortunately, countries with which the U.S. already has free trade agreements, like Australia and Chile, are projected to have prominent market shares of 11% each. Strengthening the U.S. position will be easier and faster if we work with existing partners to scale, diversify, and stabilize mineral supply chains.

These findings highlight a stark reality: if the current trajectories continue, the U.S. position in critical minerals will remain highly vulnerable. China’s extensive control of the critical mineral supply chain is only growing; China’s overseas mining investments peaked last year, reaching $24.1 billion. Maintaining access to these inputs for American manufacturers and defense purposes is crucial. To achieve this, policymakers need to embrace an all-of-the-above approach that expands domestic production, strategic international partnerships, and innovation.