Critical minerals supply chain security is drawing significant policymaker interest, with three executive orders and at least seven bills introduced this year alone. The heightened attention is due to the U.S.’s precarious position in the critical mineral market. The United States Geological Survey has designated 50 elements and minerals as critical because they are essential to economic and national security and face a high risk of supply disruption. The U.S. is a minor player in the market, projected to hold less than 2% global market share for key mineral extraction through 2030, and an even more minimal share of global processing. But thanks to rapidly growing advanced manufacturing capacity, the U.S.’s need for critical minerals is only increasing.

In contrast, China controls 60% of global production and 85% of processing capacity, which has been built and maintained through decades of subsidies, export controls, and market manipulation. They have repeatedly indicated interest in leveraging their position for economic and geopolitical gain, committing to export restrictions on dual-use inputs such as graphite, gallium, germanium, and certain rare earth minerals in recent years.

As part of its efforts to address supply chain security, the Trump administration launched a 232 investigation into the national security risks of import reliance on processed critical minerals and derivative products. To support the investigation, the Council analyzed trade data for key critical minerals—cobalt, lithium, graphite, and rare earths—to better understand the subtleties of individual critical mineral markets. We summarize our four key findings here:

- U.S. companies have already begun diversifying mineral supplies where possible.

- Diverse mineral sourcing may obscure significant exposure to Chinese market control.

- Where the U.S. is dependent upon Chinese imports, significant market manipulation can impede domestic investment.

- Where the U.S. is dependent upon Chinese imports, U.S. industry strives to invest in supply chain resiliency.

U.S. companies have already begun diversifying mineral supplies where possible…but diverse mineral sourcing may obscure significant exposure to Chinese market control.

Trade data demonstrates that U.S. imports of cobalt and lithium have already been substantially diversified toward market-oriented economies. In these minerals, we also trade considerable volumes with markets with which the U.S shares free trade agreements: Canada (cobalt) and Chile (lithium).

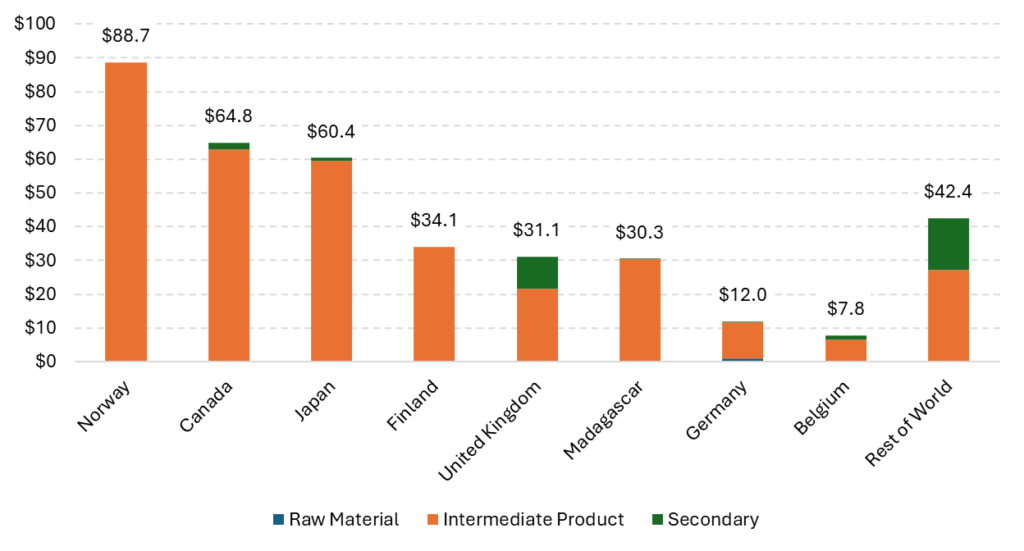

U.S. Cobalt Imports (2023 USD billions)

Net import reliance: 75%

Source: OEC

Norway, Canada, and Japan account for a combined 58% of U.S. cobalt imports. U.S. industry imports mostly intermediate products and secondary materials, reflecting the prominent position of American firms in the manufacture of more mature goods, like cobalt-based machine parts.

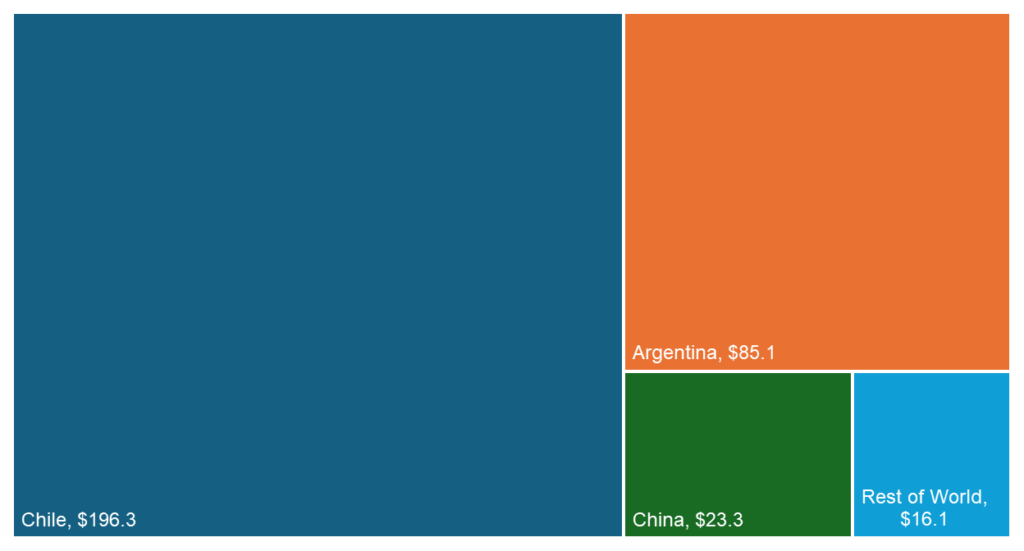

U.S. Intermediate Lithium Product Imports (2023 USD billions)

Net import reliance: 50%

Source: OEC

More than 75% of U.S. lithium imports come from resource-rich partners in the Lithium Triangle, including Chile, an FTA partner. Chile and Argentina account for 29% of global lithium production.

The U.S. has already made great strides in distancing its supply chains from more risky Chinese sources. But these trends disguise growing risk: in both cobalt and lithium, the CCP is investing in resource ownership that may ultimately destabilize the suppliers with which the U.S. trades today. In cobalt, China has significant influence on the upstream mineral market and is estimated to control 72% of the cobalt and copper mines in the Democratic Republic of the Congo, the single largest cobalt producer. In lithium, China is already involved in 6 of Argentina’s 16 active lithium projects. While the U.S. trades preferentially in some minerals with market-based economies, its exposure to Chinese market manipulation may be increasing thanks to their strategic upstream investments.

Where the U.S. is dependent upon Chinese imports, significant market manipulation can impede domestic investment…and U.S. industry strives to invest in supply chain resiliency.

Again, we examine two minerals to reflect these market dynamics: graphite and rare earth elements (REE), a group of 17 metallic elements. China is the dominant producer and processor of both minerals, and the U.S. is forced to trade considerable volumes with Chinese firms.

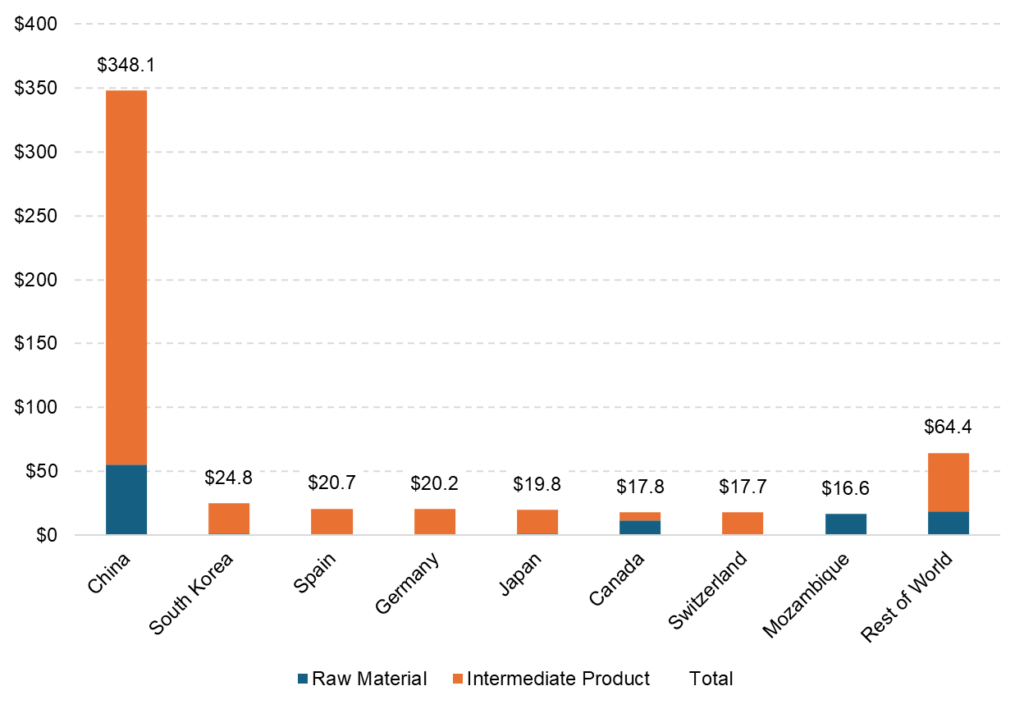

China accounts for 63% of U.S. graphite imports and is estimated to control 82% of upstream graphite materials and 90% of midstream materials. Their market position has left the U.S. and other partners exposed to the non-market practices of the CCP. Marginal trade flows with other countries limit the ability of American firms to access different sources of materials.

U.S. Raw and Intermediate Graphite Product Imports (2023 USD millions)

Net import reliance: 100%

Source: OEC

The tight control of the graphite market by the CCP impacts the ability of U.S. firms to establish a foothold in the market. Last December, the American Active Anode Material Producers (AAAMP) called for an investigation into whether China is dumping graphite anode material on the U.S. market. The Commerce Department’s preliminary determination found certain Chinese graphite imports are being unfairly subsidized and laid out a plan to implement antidumping duties up to 721%.

On the other hand, the U.S. is enjoying more success in supply chain diversification when it comes to rare earth elements (REE). Like in graphite, China is a dominant producer and refiner of REE, estimated to control 61% of upstream materials and 92% of midstream materials. Roughly 65% of U.S. REE imports came from China in 2023.

U.S. REE Imports (2023 USD millions)

Net import reliance: up to 100% on REE (element-dependent)

Source: OEC

In spite of this historic import reliance, the U.S. is expanding its REE capacity; the U.S. REE extraction and processing industry now accounts for more than 9% of global production capacity. American producers that historically relied on China for onward processing have begun stockpiling their output and investing in more mid-stream processing within the United States. In this critical mineral, American industry is successfully navigating toward vertical integration.

Through trade analysis of existing market conditions, we can understand the complexity of improving supply chain security for critical minerals. As the U.S. advances its toolkit to scale, diversify, and stabilize critical mineral supplies, it must respond to the mineral-specific market conditions; doing so will ensure that policy supports the growing domestic advanced manufacturing sector with reliable, affordable inputs.